When it comes to securing a mortgage, one of the most critical decisions you’ll face is choosing between a fixed and a floating interest rate. While fixed-rate mortgages offer the comfort of predictable payments, floating-rate mortgages—also known as adjustable-rate mortgages (ARMs)—introduce an element of unpredictability. These loans can be both enticing and intimidating, as their interest rates fluctuate with market conditions. But how exactly does a mortgage with a floating interest rate work, and is it worth the risk? Let’s explore the mechanics, benefits, and potential drawbacks of this financial instrument to help you make an informed decision.

The Mechanics of a Floating Interest Rate Mortgage

A floating interest rate mortgage is tied to a benchmark interest rate, such as the Prime Rate or the London Interbank Offered Rate (LIBOR). Unlike a fixed-rate mortgage, where the interest rate remains constant throughout the loan term, a floating rate adjusts periodically based on changes in the benchmark. This adjustment typically occurs at predefined intervals, such as every six months or annually, and is outlined in the loan agreement.

The interest rate on a floating-rate mortgage is usually expressed as the benchmark rate plus a fixed margin. For example, if the benchmark rate is 3% and the margin is 2%, your interest rate would be 5%. If the benchmark rate rises to 4%, your rate would adjust to 6%, and your monthly payments would increase accordingly. Conversely, if the benchmark rate drops, so does your interest rate, potentially lowering your payments.

To protect borrowers from extreme fluctuations, floating-rate mortgages often come with caps and floors. A cap limits how much the interest rate can increase during a specific period or over the life of the loan, while a floor sets a minimum rate below which it cannot fall. These safeguards provide a degree of stability, but they don’t eliminate the inherent uncertainty of a floating rate.

The Appeal of a Floating Interest Rate Mortgage

One of the primary attractions of a floating-rate mortgage is the potential for lower initial payments. These loans often start with an introductory rate that is lower than the prevailing fixed-rate mortgages. This can make them an appealing option for borrowers who plan to sell or refinance their homes within a few years, as they can take advantage of the lower payments without being exposed to long-term rate fluctuations.

Additionally, if market interest rates decline, borrowers with floating-rate mortgages can benefit from reduced payments without needing to refinance. This flexibility can be particularly advantageous in a low-interest-rate environment, where fixed-rate borrowers are locked into higher rates.

Floating-rate mortgages can also be a strategic choice for financially savvy individuals who are comfortable with risk and have a solid understanding of market trends. For example, if you anticipate that interest rates will remain stable or decrease in the near future, a floating-rate mortgage could save you money over time.

The Risks of a Floating Interest Rate Mortgage

While the potential for lower payments is enticing, floating-rate mortgages come with significant risks. The most obvious is the possibility of rising interest rates, which can lead to higher monthly payments and increased financial strain. Even with caps in place, a substantial rate hike can make your mortgage payments unaffordable, especially if your income doesn’t keep pace.

Another risk is the unpredictability of future payments. Unlike fixed-rate mortgages, where you know exactly how much you’ll pay each month, floating-rate mortgages introduce uncertainty. This can make budgeting more challenging, particularly for borrowers with tight finances or variable incomes.

Floating-rate mortgages can also be less appealing in a rising interest rate environment. If rates climb significantly, you could end up paying far more over the life of the loan than you would with a fixed-rate mortgage. This scenario can be particularly problematic for long-term borrowers who don’t plan to sell or refinance their homes in the near future.

Factors to Consider Before Choosing a Floating-Rate Mortgage

Before committing to a floating-rate mortgage, it’s essential to evaluate several factors to determine if it’s the right choice for you. First, consider your financial stability. Do you have a steady income that can accommodate potential increases in your monthly payments? If your income is variable or uncertain, a fixed-rate mortgage might provide the security you need.

Next, think about your long-term plans. If you intend to stay in your home for many years, a fixed-rate mortgage might be more suitable, as it offers stability over the long term. On the other hand, if you plan to move or refinance within a few years, a floating-rate mortgage could allow you to take advantage of lower initial payments.

It’s also crucial to assess your risk tolerance. Are you comfortable with the possibility of fluctuating payments, or do you prefer the certainty of a fixed rate? If the thought of rising interest rates keeps you up at night, a floating-rate mortgage might not be the best fit for you.

How Market Conditions Influence Floating Rates

Understanding how market conditions affect floating interest rates is key to making an informed decision. Floating rates are closely tied to broader economic trends, such as inflation, central bank policies, and global financial markets. For example, if the central bank raises interest rates to combat inflation, floating-rate mortgages will likely become more expensive.

Keeping an eye on economic indicators can help you anticipate changes in interest rates. However, predicting market movements with certainty is nearly impossible, which is why floating-rate mortgages carry inherent risk. If you’re considering this type of loan, it’s wise to stay informed about economic trends and consult with financial experts to gauge the potential impact on your mortgage.

Alternatives to Floating-Rate Mortgages

If the uncertainty of a floating-rate mortgage gives you pause, there are alternatives worth exploring. One option is a hybrid adjustable-rate mortgage, which combines features of both fixed and floating rates. These loans typically offer a fixed rate for an initial period, such as five or seven years, before transitioning to a floating rate. This structure provides stability in the short term while allowing for potential savings if interest rates decline.

Another alternative is a fixed-rate mortgage with the option to refinance. If interest rates drop significantly, you can refinance your loan to take advantage of the lower rates. While this approach requires paying refinancing fees, it offers the security of predictable payments during the initial loan term.

Is a Floating Interest Rate Mortgage Worth It?

The decision to choose a floating-rate mortgage ultimately depends on your financial situation, risk tolerance, and long-term plans. If you’re confident that you can handle potential rate increases and plan to sell or refinance before the introductory period ends, a floating-rate mortgage might be a worthwhile option. It can provide lower initial payments and flexibility in a favorable market environment.

However, if you prefer stability and predictability, a fixed-rate mortgage may be a better fit. Fixed-rate loans offer the peace of mind of knowing exactly what your payments will be for the entire loan term, making them ideal for long-term homeowners or those with fixed incomes.

It’s also important to consider your financial resilience. Can you afford higher payments if interest rates rise? Do you have a contingency plan in case of financial hardship? Answering these questions honestly can help you determine whether a floating-rate mortgage aligns with your financial goals and risk tolerance.

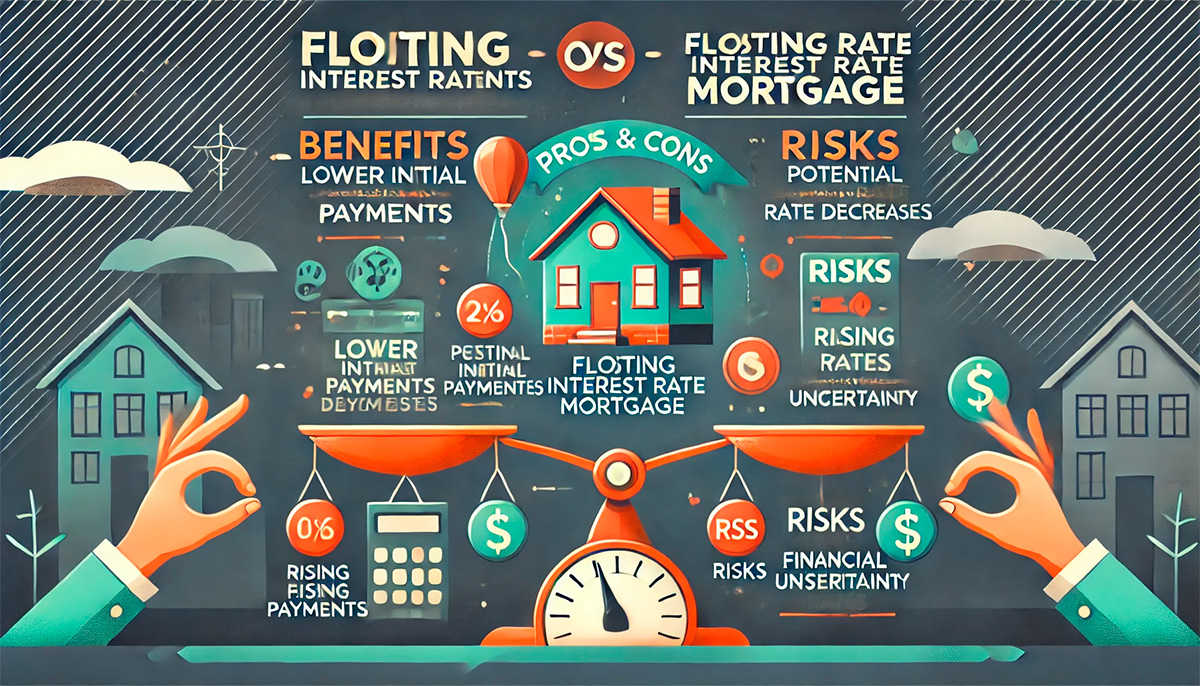

Conclusion: Weighing the Pros and Cons

A mortgage with a floating interest rate is a double-edged sword. It offers the potential for lower initial payments and flexibility in a declining rate environment but carries the risk of higher payments and financial uncertainty if rates rise. Understanding how these loans work and carefully evaluating your financial situation are crucial steps in making an informed decision.

Before committing to a floating-rate mortgage, take the time to research market trends, consult with financial advisors, and compare different loan options. Remember, the right choice isn’t just about securing the lowest rate—it’s about finding a mortgage that supports your long-term financial well-being. Whether you opt for the stability of a fixed rate or the flexibility of a floating rate, the key is to choose wisely and plan for the future.

Ultimately, the decision comes down to your unique circumstances and goals. By weighing the pros and cons and considering your financial resilience, you can make a choice that aligns with your needs and sets you on the path to homeownership with confidence.